When you’ve suffered property damage—whether from a hurricane, hailstorm, burst pipe, or fire—you expect your insurance company to keep its promise. After all, you’ve paid premiums faithfully for years. Yet for many Houston homeowners and business owners, the reality is a cold denial letter in the mail.

Having your claim denied can feel devastating. Suddenly, instead of receiving help to rebuild, you’re left with mounting repair bills and nowhere to turn. This is where working with a Houston property damage attorney can make all the difference.

This comprehensive guide explains why insurance claims get denied, what steps you should take immediately, the legal rights you have under Texas law, and how to fight back to secure the compensation you deserve.

Why Insurance Companies Deny Claims

Insurance companies are businesses. Their goal is to protect profits—not necessarily to pay out claims in full. Denials are one of their most effective cost-saving strategies. Below are some of the most common reasons insurers cite:

Policy Exclusions

Insurance policies are filled with exclusions. For example, flood damage may not be covered under a standard homeowner’s policy, requiring separate flood insurance. Insurers often rely on these exclusions to avoid paying.

👉 Related Reading: Understanding Home Fire Claims

Alleged Late Filing

Texas insurance policies require “prompt” reporting. Insurers may deny a claim by arguing you waited too long—even when you filed as soon as you discovered the damage.

Insufficient Documentation

A lack of evidence is a common excuse. Without detailed photos, receipts, or contractor estimates, insurers may claim they can’t verify your loss.

Wear and Tear vs. Sudden Damage

If a storm damages your roof, insurers may say the problem was pre-existing wear and tear. This is especially common in hail or hurricane damage claims.

Misrepresentation Accusations

Insurers sometimes allege that you misrepresented information either on your policy application or claim form. These accusations can be intimidating, but they’re often baseless.

Steps to Take After Receiving a Denial

A denial is not the end of your claim—it’s the beginning of the fight. Here’s how to respond effectively:

Step 1: Read the Denial Letter Thoroughly

Texas law requires insurance companies to explain why they are denying coverage. Compare the letter to your policy’s language. Many denials misapply exclusions.

Step 2: Collect Strong Evidence

You’ll need proof that your loss is covered. Consider gathering:

- Photos and videos of the damage from multiple angles

- Before-and-after comparisons (e.g., old property photos vs. current damage)

- Repair estimates from licensed contractors

- Weather reports documenting storm conditions

- Expert opinions (e.g., engineers or roofers stating cause of damage)

👉 Related Reading: Wind and Hail Damage Claims in Texas

Step 3: File a Written Appeal

Insurers often allow internal appeals. Submit your evidence along with a detailed letter explaining why your claim should be covered. Always cite your policy language directly.

Step 4: Consult a Houston Property Damage Attorney

If the insurer refuses to reconsider, you need legal backup. A property damage attorney can pressure insurers by filing a bad faith claim or taking the case to court.

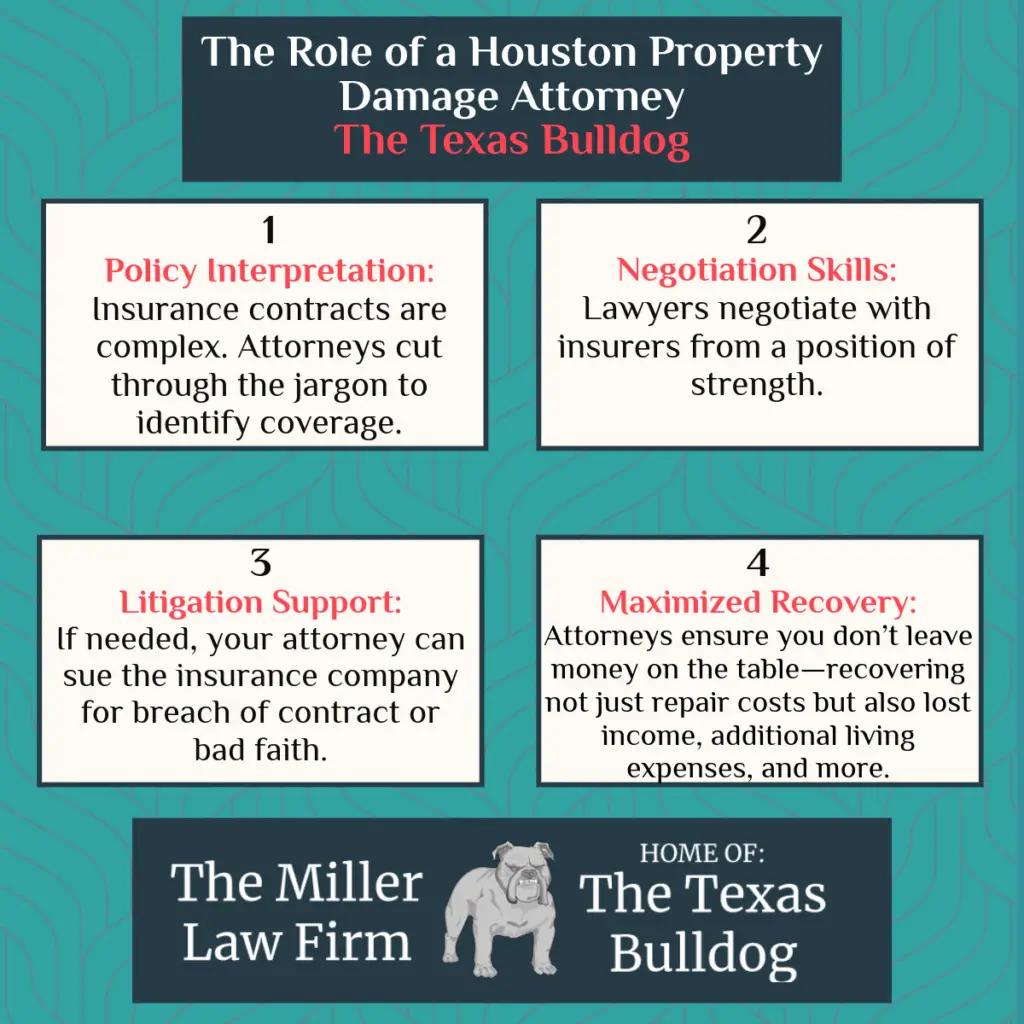

The Role of a Houston Property Damage Attorney

Insurance companies employ teams of lawyers whose only job is to protect corporate profits. Without an attorney on your side, you’re fighting with one hand tied behind your back.

👉 Related Reading: Property Damage Claims in Houston

Texas Law: Protections for Policyholders

Texas offers strong legal protections against unfair insurance practices. These include:

Texas Insurance Code § 541

This law prohibits insurers from engaging in unfair or deceptive acts, such as misrepresenting coverage or refusing to pay valid claims.

Texas Prompt Payment of Claims Act (§ 542)

Insurers must investigate and pay claims promptly. If they delay without reason, they may owe penalties, including interest on unpaid amounts.

Common Law Bad Faith

Even without a statute, Texas courts recognize a duty of “good faith and fair dealing.” If an insurer wrongfully denies a claim, policyholders may recover extra damages.

Denied Insurance Claim: Your Next Move

| Denial Reason | Insurer’s Excuse | How to Respond | Attorney’s Role |

|---|---|---|---|

| Policy Exclusion | “Not covered by your policy” | Review policy language | Argue coverage in court if misapplied |

| Late Filing | “Filed too late” | Show proof of timely notice | Argue delay was reasonable under law |

| Insufficient Documentation | “Not enough proof” | Submit photos & receipts | Build expert-backed evidence |

| Disputed Cause | “Pre-existing wear & tear” | Get contractor/engineer report | Hire independent adjusters, experts |

Real-World Examples

Example 1: Storm Damage Denial

A Houston family filed a claim after Hurricane Harvey damaged their home. The insurer blamed pre-existing wear. With attorney help, expert reports proved storm damage, leading to full payout plus attorney’s fees.

Example 2: Fire Loss Dispute

A business owner’s fire claim was denied for “policy exclusions.” After review, the exclusion was misapplied. The denial was overturned, securing compensation for building repairs and business interruption.

Example 3: Water Damage Claim

A burst pipe flooded a property. The insurer delayed payment for months. Under the Texas Prompt Payment Act, the attorney secured the claim value plus interest penalties.

How Attorneys Build Strong Cases

A Houston property damage attorney uses multiple strategies:

- Independent Adjusters: To challenge the insurer’s assessment.

- Expert Witnesses: Engineers, meteorologists, and contractors confirm the true cause of damage.

- Bad Faith Claims: Attorneys may sue for more than just the policy benefits if insurers acted unfairly.

- Aggressive Negotiation: Insurers often settle rather than risk trial.

Timeline for Fighting a Denied Claim

- Initial Denial: Usually within 15–30 days of filing.

- Internal Appeal: 30–60 days to resubmit documentation.

- Attorney Review: As soon as denial is issued, ideally within weeks.

- Litigation: A lawsuit can take 6 months to several years, depending on complexity.

Steps to Fight a Denied Insurance Claim:

- Read your denial letter carefully.

- Review your policy and compare coverage.

- Collect strong evidence (photos, reports, receipts).

- File a detailed written appeal.

- Contact a Houston property damage attorney.

- Explore mediation, negotiation, or litigation.

FAQ – People Also Ask

Q1: Can I sue my insurance company for denying my claim?

Yes. If the insurer acted in bad faith, you can file a lawsuit. Texas law allows recovery of your policy benefits plus additional damages.

Q2: What should I do immediately after a denial?

Don’t panic. Read the denial letter, gather more evidence, and consider appealing in writing. If that fails, call an attorney.

Q3: How long do I have to appeal?

Most insurers require appeals within 30–60 days. Always check your denial letter for exact deadlines.

Q4: What is “bad faith”?

Bad faith occurs when insurers misrepresent policies, fail to investigate, delay payment, or deny valid claims without reason.

Q5: Should I hire a lawyer right away?

For major losses—like storm, fire, or water damage—yes. Attorneys dramatically increase your chances of success.

Q6: How much does a Houston property damage attorney cost?

Most work on contingency. You pay nothing unless they win your case.

Q7: Will hiring an attorney speed things up?

Often, yes. Insurance companies know attorneys can sue, so they tend to respond more quickly.

Q8: Can pre-existing damage be excluded?

Yes, but the insurer must prove it. Expert testimony often disproves these excuses.

Q9: What evidence is strongest in appeals?

Independent contractor reports, before-and-after photos, and weather data carry significant weight.

Q10: What if my claim was underpaid instead of denied?

You can challenge underpayment just like a denial. Attorneys regularly expose hidden costs insurers ignore.

Conclusion & Call to Action

Don’t let an insurance company’s denial stop you from rebuilding your life. Whether your home, business, or property suffered damage, you have rights under Texas law.

At The Miller Law Firm – Texas Bulldog, we fight for policyholders every day. As your Houston property damage attorney, we know how to push back against unfair denials and win results.

📞 Call 713-572-3333 now for a free consultation.

The Miller Law Firm has won hundreds of millions for our clients and is well known as one of the best firms in Houston. However, don’t just take our word for it. Check out our 100+⭐ ⭐ ⭐ ⭐ ⭐ 5 Star Reviews on Google!