Texas Uninsured and Underinsured Motorist Guide: What Happens If the Other Driver Has No Insurance?

Part of the Texas Injury Law Library

The Texas Injury Law Library is a collection of educational resources published by The Miller Law Firm, home of The Texas Bulldog. These guides explain important Texas personal injury laws, insurance issues, medical billing concerns, and legal concepts in plain English.

This guide focuses on uninsured and underinsured motorist (UM/UIM) coverage in Texas, including what happens when an at-fault driver has little or no insurance, how UM/UIM claims work, what damages may be covered, and how these claims can affect accident compensation.

Last Updated: June 2026

Quick Answer

Uninsured motorist (UM) and underinsured motorist (UIM) coverage can help pay for injuries and damages when the driver who caused an accident has no insurance or does not carry enough insurance to fully compensate the injured person.

Texas insurance companies must offer UM/UIM coverage to drivers, but policyholders may reject the coverage in writing. If UM/UIM coverage is included in a policy, it may provide compensation for medical expenses, lost wages, pain and suffering, vehicle damage, and other losses arising from a covered accident.

Many accident victims are surprised to learn that recovering compensation through a UM/UIM claim often involves negotiating with their own insurance company. Understanding how UM/UIM coverage works, what damages may be available, and how insurers evaluate these claims can be an important part of protecting your rights after a serious accident.

Table of Contents

- What Is Uninsured Motorist Coverage in Texas?

- What Is Underinsured Motorist Coverage?

- Is UM/UIM Coverage Required in Texas?

- How Does UM/UIM Coverage Work After an Accident?

- What Happens If the At-Fault Driver Has No Insurance?

- What Happens If the At-Fault Driver Does Not Have Enough Insurance?

- Adam Miller Explains Underinsured Motorist Claims

- What Damages Can UM/UIM Coverage Pay?

- Does Comparative Fault Affect a UM/UIM Claim?

- How Do Insurance Companies Evaluate UM/UIM Claims?

- Common Mistakes Accident Victims Make

- UM/UIM Coverage vs. Liability Insurance

- Frequently Asked Questions

- Sources and Legal Authorities

- Attorney Insight

- Questions About UM/UIM Claims?

What Is Uninsured Motorist Coverage in Texas?

Uninsured motorist (UM) coverage is a type of automobile insurance that may provide compensation when an accident is caused by a driver who does not carry liability insurance. In Texas, uninsured motorist coverage is intended to protect responsible drivers from the financial consequences of being injured by someone who failed to maintain the insurance required by law.

According to the Texas Department of Insurance, uninsured motorist coverage may help pay for medical expenses, lost wages, pain and suffering, vehicle damage, and other losses resulting from a covered accident.

UM coverage may also apply in certain hit-and-run accidents when the at-fault driver cannot be identified. Because the responsible driver cannot be located, injured individuals may be forced to rely on their own insurance coverage to seek compensation for their losses.

Many drivers assume that every motorist on Texas roads carries insurance. Unfortunately, that is not always the case. Even though Texas law requires drivers to maintain minimum liability insurance coverage, uninsured drivers continue to be involved in accidents throughout the state each year.

For accident victims facing medical bills, lost income, and other financial challenges, uninsured motorist coverage can serve as an important safety net when the at-fault driver lacks insurance coverage.

Understanding what uninsured motorist coverage does—and does not cover—is often the first step in determining what options may be available after a serious accident.

What Is Underinsured Motorist Coverage?

Underinsured motorist (UIM) coverage may provide compensation when the driver who caused an accident has insurance, but the available policy limits are not sufficient to fully cover the injured person’s damages.

This situation is more common than many drivers realize. Texas law requires drivers to carry minimum liability insurance, but serious accidents often result in damages that far exceed those minimum coverage limits. Medical bills, lost income, future treatment costs, pain and suffering, and other losses can quickly surpass the amount of insurance available from the at-fault driver.

For example, a driver may carry the Texas minimum liability limits, but a serious crash could result in damages worth substantially more than the available coverage. In that situation, underinsured motorist coverage may help bridge the gap between the at-fault driver’s insurance and the injured person’s actual losses.

Unlike uninsured motorist coverage, which applies when the at-fault driver has no insurance at all, underinsured motorist coverage applies when insurance exists but is insufficient to fully compensate the injured person.

Many accident victims discover the importance of UIM coverage only after learning that the at-fault driver’s insurance policy is inadequate to cover the damages caused by the collision. For that reason, underinsured motorist coverage is often considered one of the most valuable optional coverages available under a Texas automobile insurance policy.

Is UM/UIM Coverage Required in Texas?

According to the Texas Department of Insurance, Texas insurance companies are required to offer uninsured and underinsured motorist coverage to drivers when they purchase an automobile insurance policy. However, Texas drivers are not required to purchase the coverage.

Under Texas law, UM/UIM coverage is generally included unless the policyholder rejects it in writing. As a result, many drivers may have uninsured or underinsured motorist coverage without realizing it, while others may have declined the coverage years earlier when purchasing or renewing their policy.

Because UM/UIM coverage is optional, policy limits and available benefits can vary significantly from one insurance policy to another. Some drivers purchase only the minimum available coverage, while others elect higher limits for additional protection.

Many insurance professionals consider UM/UIM coverage one of the most valuable optional coverages available because it helps protect policyholders from the financial consequences of accidents involving uninsured or underinsured drivers.

Before assuming UM/UIM coverage is available, accident victims should review their insurance policy declarations page and policy documents to determine whether the coverage was purchased and what limits may apply.

Understanding whether UM/UIM coverage exists is often one of the first questions that must be answered after learning that the at-fault driver has little or no insurance.

How Does UM/UIM Coverage Work After an Accident?

Many drivers assume that recovering compensation through uninsured or underinsured motorist coverage is a simple process because the claim is being made through their own insurance company. In reality, UM/UIM claims often involve investigations, negotiations, documentation requirements, and disputes regarding the value of the claim.

Before UM/UIM benefits become available, it is typically necessary to determine whether the at-fault driver was uninsured or whether the available liability insurance is insufficient to fully compensate the injured person. Insurance companies often review police reports, witness statements, medical records, insurance policies, and other evidence before evaluating a UM/UIM claim.

Once coverage issues have been addressed, the insurance company may evaluate the injured person’s damages. This can include medical expenses, lost income, future treatment costs, pain and suffering, physical impairment, and other accident-related losses.

Although the claim is being made under the injured person’s own policy, the insurance company may still challenge liability, dispute damages, question medical treatment, or disagree with the amount of compensation being requested. For that reason, UM/UIM claims often resemble traditional personal injury claims in many respects.

Understanding how insurance companies evaluate accident claims can help injured individuals better navigate the process. Our Insurance Game resource explains many of the strategies insurers commonly use when reviewing injury claims and settlement demands.

Because every accident is different, the specific procedures and requirements for a UM/UIM claim will depend on the insurance policy, the facts of the accident, and the damages involved.

What Happens If the At-Fault Driver Has No Insurance?

When the driver who caused an accident has no liability insurance, recovering compensation can become significantly more difficult. Even though Texas law requires drivers to maintain minimum liability insurance coverage, uninsured drivers continue to cause accidents throughout the state every year.

Without uninsured motorist coverage, an injured person may be forced to pursue compensation directly from the at-fault driver. In many cases, however, uninsured drivers have limited financial resources, making it difficult to collect a judgment even if liability is clear.

If uninsured motorist coverage is available, the injured person’s own insurance policy may provide an alternative source of compensation. Depending on the policy and the circumstances of the accident, UM coverage may help pay for medical expenses, lost wages, pain and suffering, vehicle damage, and other covered losses.

Hit-and-run accidents can create similar challenges. When the at-fault driver cannot be identified, injured individuals may need to rely on uninsured motorist coverage to pursue compensation for their injuries and damages.

Because insurance companies often investigate liability, damages, and coverage issues before paying UM benefits, accident victims should preserve evidence whenever possible. Police reports, photographs, witness statements, medical records, and vehicle damage documentation may all play an important role in supporting a claim.

For many Texans, uninsured motorist coverage provides important financial protection against the risk of being seriously injured by a driver who failed to carry insurance.

What Happens If the At-Fault Driver Does Not Have Enough Insurance?

In many serious accidents, the at-fault driver carries insurance but does not have enough coverage to fully compensate the injured person. This is the situation that underinsured motorist (UIM) coverage is designed to address.

Texas drivers are only required to carry minimum liability insurance limits. While those minimum limits may be sufficient for minor accidents, they are often inadequate when a crash results in significant injuries, surgery, extended medical treatment, lost income, or long-term physical limitations.

For example, an injured person may incur medical expenses, lost wages, and other damages that greatly exceed the amount of insurance available under the at-fault driver’s policy. Once those policy limits have been exhausted, underinsured motorist coverage may provide an additional source of compensation, depending on the terms and limits of the injured person’s policy.

Determining whether a driver is truly underinsured often requires a careful evaluation of the available liability coverage, the injured person’s damages, and the applicable UM/UIM policy limits. As a result, underinsured motorist claims can be more complex than many accident victims initially expect.

Because serious injury claims frequently involve damages that exceed minimum insurance limits, underinsured motorist coverage can play an important role in helping injured Texans recover compensation that might otherwise be unavailable.

Understanding how underinsured motorist claims work is especially important because many drivers do not discover the limits of the at-fault driver’s insurance until after substantial medical treatment has already occurred.

Adam Miller Explains Underinsured Motorist Claims

Many Texas drivers carry only the minimum amount of liability insurance required by law. When serious injuries exceed those policy limits, underinsured motorist coverage may become an important source of compensation. In the video below, Adam Miller explains how underinsured motorist claims can arise after a serious accident.

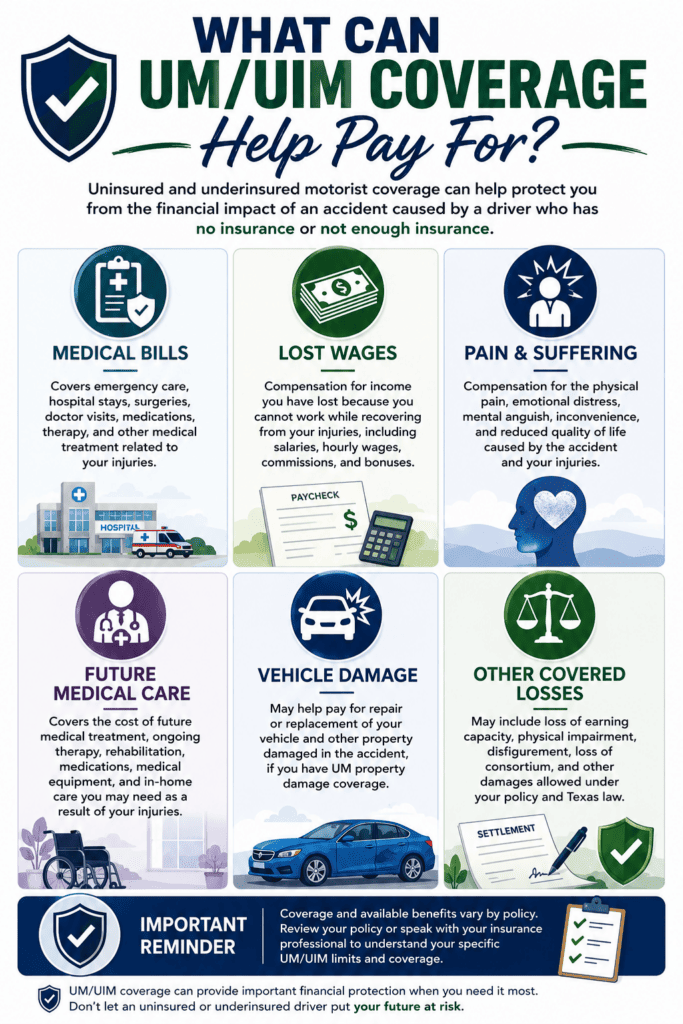

What Damages Can UM/UIM Coverage Pay?

The damages available through uninsured and underinsured motorist coverage often depend on the terms of the insurance policy, the nature of the injuries, and the facts of the accident. In many cases, UM/UIM coverage is intended to place the injured person in a similar position to what would have been available if the at-fault driver carried adequate liability insurance.

Depending on the policy and circumstances involved, UM/UIM claims may include compensation for medical expenses, lost wages, loss of earning capacity, physical impairment, pain and suffering, mental anguish, and other accident-related damages.

When a settlement or insurance recovery involves substantial medical treatment, accident victims may also encounter hospital lien issues. Our Texas Hospital Liens Guide explains how certain medical providers may seek reimbursement from settlement proceeds.

Vehicle damage may also be covered under certain UM property damage provisions. However, coverage limits, deductibles, exclusions, and policy language can affect what benefits are ultimately available.

Insurance companies often evaluate the same types of evidence that appear in traditional personal injury claims, including medical records, treatment history, diagnostic imaging, physician opinions, wage documentation, and evidence regarding how the injuries affect daily activities.

Because UM/UIM claims can involve substantial damages, disputes sometimes arise regarding the value of the claim. Insurance companies may challenge the extent of injuries, question future medical treatment recommendations, or disagree with the amount of compensation being sought.

Understanding the categories of damages that may be available through UM/UIM coverage can help accident victims better evaluate their claim and understand what compensation may be available after a serious accident.

Does Comparative Fault Affect a UM/UIM Claim?

Yes. Comparative fault can affect uninsured and underinsured motorist claims in much the same way it affects other Texas personal injury claims. Even when UM/UIM coverage is available, the amount of compensation an injured person may recover can depend on the degree of fault assigned to each party involved in the accident.

Texas follows a modified comparative fault system, sometimes referred to as the 51% rule. Under this rule, an injured person may generally recover compensation if they are 50% or less responsible for the accident. However, the amount of compensation may be reduced by the percentage of fault assigned to them.

For example, if an accident victim suffers $100,000 in damages but is found to be 20% responsible for the crash, the potential recovery may be reduced to $80,000. If the injured person is determined to be more than 50% responsible, compensation may be barred entirely under Texas law.

Insurance companies frequently evaluate fault issues when reviewing UM/UIM claims. Because the claim is often being made against the injured person’s own insurance policy, many accident victims are surprised to learn that their insurer may still dispute liability or argue that they share responsibility for the collision.

Understanding how comparative fault works can be critical when evaluating any UM/UIM claim. For a more detailed explanation of Texas fault allocation rules, visit our Texas Comparative Fault Guide: Understanding the 51% Rule.

Because fault disputes can significantly affect compensation, accident victims should preserve evidence and carefully document the circumstances surrounding the crash whenever possible.

How Do Insurance Companies Evaluate UM/UIM Claims?

Many accident victims assume that filing a claim under their own uninsured or underinsured motorist coverage will be easier than pursuing compensation from another driver’s insurance company. While UM/UIM coverage can provide valuable protection, insurance companies often evaluate these claims just as carefully as any other personal injury claim.

Insurers typically review a wide range of evidence before determining whether benefits are owed and how much compensation may be appropriate. This often includes police reports, witness statements, photographs, medical records, treatment history, diagnostic imaging, employment records, and documentation regarding the injured person’s damages.

Insurance companies may also examine whether the accident occurred as reported, whether the injuries were caused by the collision, whether medical treatment was reasonable and necessary, and whether the claimed damages are supported by the available evidence.

Because UM/UIM claims frequently involve significant financial exposure, insurers may dispute liability, challenge the severity of injuries, question future medical treatment recommendations, or argue that certain damages are unrelated to the accident. These are many of the same issues that arise in traditional personal injury claims.

Understanding how insurance companies evaluate claims can help accident victims better prepare for the process. Our Insurance Game resource explains how insurers investigate accidents, evaluate injuries, calculate settlement value, and negotiate claims after a Texas accident.

Because every claim is unique, the strength of the evidence often plays a significant role in determining how a UM/UIM claim is ultimately resolved.

Common Mistakes Accident Victims Make

Assuming UM/UIM Coverage Is Automatic

Many drivers believe they have uninsured and underinsured motorist coverage without verifying their policy. Because Texas drivers may reject UM/UIM coverage in writing, it is important to review policy documents and declarations pages to determine what coverage actually exists.Waiting Too Long to Report the Claim

Insurance policies often contain notice requirements and deadlines. Delaying the reporting of a UM/UIM claim can create unnecessary complications and may affect the insurer’s investigation.Related Guide

Reporting a UM/UIM claim to your insurance company is important, but it is also essential to understand that insurance policy notice requirements and the Texas statute of limitations are not the same thing. Even if a claim is being investigated or negotiated, you may still have a legal deadline to file a lawsuit. Learn more in our Texas Statute of Limitations Guide.

Assuming Your Insurance Company Will Automatically Agree With You

Although a UM/UIM claim is typically made under your own policy, the insurance company may still investigate liability, evaluate damages, and dispute aspects of the claim. Accident victims should not assume that compensation will be automatically approved simply because the claim involves their own insurer.Failing to Document Injuries and Damages

Medical records, photographs, wage documentation, repair estimates, and other evidence can play an important role in establishing the value of a UM/UIM claim. Thorough documentation often strengthens the claim and reduces disputes regarding damages.Accepting a Settlement Before Understanding the Full Extent of Injuries

Serious injuries may require ongoing treatment, future medical care, or extended recovery periods. Settling a claim too early can make it difficult to account for losses that become apparent later.Ignoring Comparative Fault Issues

Insurance companies may argue that an injured person shares responsibility for the accident. Because fault allocation can directly affect compensation, accident victims should understand how Texas comparative fault rules may apply to their claim. By understanding these common mistakes, drivers can better protect their rights and make more informed decisions when pursuing uninsured or underinsured motorist benefits after a Texas accident.UM/UIM Coverage vs. Liability Insurance

Many drivers are familiar with liability insurance because Texas law requires motorists to carry minimum liability coverage. However, liability insurance and uninsured/underinsured motorist coverage serve very different purposes.

| Liability Insurance | UM/UIM Coverage |

|---|---|

| Protects other people when you cause an accident. | Protects you when the at-fault driver has little or no insurance. |

| Required by Texas law. | Must be offered by insurers but may be rejected in writing. |

| Pays damages owed to injured third parties. | May pay damages owed to you after a covered accident. |

| Coverage limits depend on the policy purchased. | Coverage limits depend on the UM/UIM limits selected. |

| Designed to protect the public from negligent drivers. | Designed to protect policyholders from uninsured and underinsured drivers. |

One of the most common misconceptions is that liability insurance automatically protects a driver from every accident-related loss. In reality, liability coverage primarily protects others when the policyholder causes a crash. UM/UIM coverage exists to help protect the policyholder when another driver fails to carry adequate insurance.

Because uninsured and underinsured drivers remain a reality on Texas roads, many insurance professionals consider UM/UIM coverage one of the most important optional protections available under an automobile insurance policy.

Understanding the difference between liability insurance and UM/UIM coverage can help drivers make more informed decisions when purchasing insurance and evaluating their options after a serious accident.

Frequently Asked Questions About Texas UM/UIM Coverage

What does UM/UIM stand for?

UM stands for uninsured motorist coverage, while UIM stands for underinsured motorist coverage. Both types of coverage may help protect drivers when the at-fault driver lacks adequate insurance.

Is uninsured motorist coverage required in Texas?

No. Texas insurance companies must offer UM/UIM coverage, but drivers may reject the coverage in writing.

What is the difference between uninsured and underinsured motorist coverage?

Uninsured motorist coverage generally applies when the at-fault driver has no insurance. Underinsured motorist coverage may apply when the at-fault driver has insurance, but the available policy limits are insufficient to fully compensate the injured person.

Can I file a UM/UIM claim against my own insurance company?

Yes. UM/UIM claims are typically made through the injured person’s own automobile insurance policy.

Does UM/UIM coverage pay for pain and suffering?

Depending on the policy and circumstances involved, UM/UIM claims may include compensation for pain and suffering as well as other accident-related damages.

Does UM/UIM coverage pay for medical bills?

In many cases, UM/UIM coverage may provide compensation for medical expenses resulting from a covered accident.

Does UM/UIM coverage cover lost wages?

Lost income and other economic damages may be recoverable through a UM/UIM claim depending on the facts of the case and applicable policy limits.

What happens if the at-fault driver leaves the scene?

Certain hit-and-run accidents may qualify for uninsured motorist coverage, although specific requirements often apply.

Can my insurance company deny a UM/UIM claim?

Insurance companies may dispute liability, damages, coverage issues, or other aspects of a claim. Each claim is evaluated based on the available evidence and policy language.

Does comparative fault affect a UM/UIM claim?

Yes. Texas comparative fault rules may reduce compensation when an injured person shares responsibility for the accident.

How do I know if I have UM/UIM coverage?

The best way to determine whether UM/UIM coverage exists is to review your insurance declarations page and policy documents or contact your insurance carrier.

Can I sue an uninsured driver in Texas?

In some situations, legal action against the uninsured driver may be possible. However, recovering compensation can be difficult if the driver has limited assets or financial resources.

Does UM/UIM coverage apply to truck accidents?

Yes. UM/UIM coverage may apply when a truck accident involves an uninsured or underinsured at-fault party and the policy requirements are satisfied.

Does UM/UIM coverage apply to motorcycle accidents?

It can. Coverage depends on the policy involved and the facts of the accident.

Why is UM/UIM coverage important?

UM/UIM coverage can provide valuable financial protection when the at-fault driver has little or no insurance available to compensate accident victims for their injuries and losses.

Sources and Legal Authorities

This guide is intended to provide a plain-English explanation of uninsured and underinsured motorist coverage in Texas. The following statutes, government resources, and industry authorities may be helpful for readers seeking additional information regarding UM/UIM coverage, automobile insurance requirements, and accident-related claims.

Texas Statutes

Texas Government Resources

National Insurance and Safety Resources

Because insurance laws, policy language, and claim procedures can vary, readers should consult the current version of applicable statutes, insurance policies, and legal authorities when researching a specific UM/UIM issue.

Attorney Insight

One of the most common surprises for accident victims is learning that uninsured and underinsured motorist claims are often disputed even though the claim is being made under their own insurance policy. Many people assume their insurance company will automatically accept their position regarding liability, injuries, and damages. In reality, insurers frequently conduct detailed investigations before evaluating a UM/UIM claim.

Another issue we frequently see is drivers discovering they rejected UM/UIM coverage years earlier without fully understanding the consequences. After a serious accident involving an uninsured or underinsured driver, many people realize how valuable this coverage can be.

Because Texas minimum liability insurance limits may be insufficient to cover serious injuries, UM/UIM coverage often becomes an important source of compensation in significant accident cases. Understanding your available insurance coverage before an accident occurs can help avoid unpleasant surprises later.

Whether an accident involves an uninsured driver, inadequate insurance limits, or a disputed UM/UIM claim, understanding how coverage works is an important step toward protecting your rights and evaluating your options after a serious crash.

Questions About UM/UIM Claims?

Uninsured and underinsured motorist coverage can play a critical role when the driver who caused an accident has little or no insurance available. Understanding how UM/UIM coverage works, what damages may be available, and how insurance companies evaluate these claims can help accident victims make more informed decisions after a serious crash.

If you have questions about uninsured motorist coverage, underinsured motorist claims, insurance disputes, medical bills, or accident compensation, contact The Miller Law Firm, home of The Texas Bulldog.

You may also find these Texas Injury Law Library resources helpful:

- Texas Comparative Fault Guide: Understanding the 51% Rule

- Texas Hospital Liens Guide: How Medical Bills Affect Your Settlement

- How the Insurance Game Works After a Texas Accident

- What It Costs to Hire a Car Accident Lawyer in Houston

Call 713-572-3333 for a free consultation.

The Miller Law Firm, home of The Texas Bulldog, proudly represents injury victims throughout Houston and across Texas.