Introduction

Most people assume insurance is a promise: you pay your premiums, and your insurer protects you when disaster strikes. But in Texas, that promise often comes with fine print—and in some cases, consequences.

One of the biggest surprises for policyholders is discovering that after you file a property damage claim, your insurance company may decide not to renew your policy. Suddenly, the company you trusted turns its back on you, right when you need coverage the most.

That’s why so many Texans search for attorneys for property damage after a claim goes sideways. Whether your claim was underpaid, delayed, or followed by a non-renewal notice, you deserve answers—and someone who knows how to hold insurers accountable.

This guide walks you through why insurers drop people, what Texas law allows, the red flags to watch for, how we fight back, and real steps to protect yourself.

Table of Contents

- What Does “Being Dropped” Really Mean?

- Can Insurance Drop You After a Claim?

- Texas Insurance Laws You Should Know

- Graph: Non-Renewal Rates in Texas

- Red Flags You’re About to Be Dropped

- Common Reasons Insurers Drop Policyholders

- When Insurance Companies Cannot Drop You

- Why Property Damage Claims Trigger More Drops

- Case Study: How We Forced an Insurer to Reverse a Non-Renewal

- How Much Does a Property Damage Attorney Cost?

- Property Damage Types We Handle

- Demand Letter Breakdown: What We Send to Insurers

- Checklist: What To Bring to Your Free Case Review

- Download Our Free Property Damage eBook

- How to Protect Yourself After Filing a Claim

- When to Call Attorneys for Property Damage

- About Adam — The Texas Bulldog

- Google Reviews

- Houston Property Damage Lawyer | Fighting Insurance Claim Denials

- Frequently Asked Questions for Attorneys for Property Damage

- Google Map

What Does “Being Dropped” Really Mean?

Insurers rarely say, “We’re dropping you.”

They use gentler language:

- “We will not be renewing your policy.”

- “Your home no longer meets underwriting requirements.”

- “Due to previous claims, we cannot extend coverage.”

Whatever words they choose, the outcome is the same:

You lose coverage.

For homeowners, this can violate your mortgage agreement.

For drivers, it can make you illegal to drive.

This is why people immediately search for attorneys for property damage—because a non-renewal is not just an inconvenience. It’s a financial emergency.

Can Insurance Drop You After a Claim?

Short answer: Yes — but only under certain conditions.

In Texas, an insurer can non-renew your policy after the first 12 months, but the reason must be legally justified.

Not-at-fault claims?

Weather damage?

A single freak accident?

These cannot legally justify dropping you.

Unfortunately, insurers often push the limits of what’s allowed, expecting homeowners and drivers not to fight back.

Texas Insurance Laws You Should Know

Knowing the law helps you spot misconduct.

Texas Insurance Code Chapter 541 — Bad Faith

Insurers must treat customers fairly. If they intentionally deny or delay your claim, you may be entitled to damages.

Texas Insurance Code Chapter 542 — Prompt Payment of Claims

Insurers must follow strict deadlines:

- Acknowledge a claim within 15 days

- Decide within 15–45 days

- Pay promptly

If they violate the timeline, they must pay penalties.

Texas Insurance Code — Non-Renewal Rules

Insurers cannot:

- Drop you in the first 12 months

- Drop you for weather-related claims

- Drop you for claims older than 3 years

If they do, we challenge it immediately.

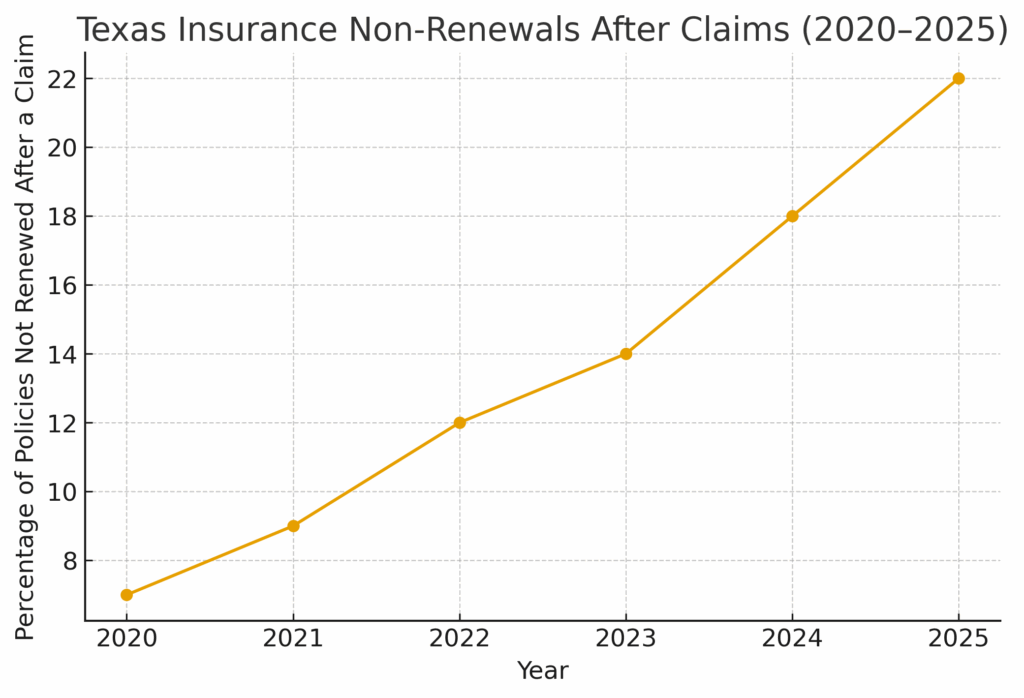

Graph: Insurance Non-Renewal Rates in Texas

Texas Insurance Non-Renewals After Claims (2020–2025)

A clear upward trend shows insurers dropping more Texans every year.

Red Flags You’re About to Be Dropped

If you see any of the following, call us immediately:

- Adjuster suddenly stops responding

- A surprise “reinspection” is ordered

- They start asking for excessive paperwork

- You receive letters mentioning “underwriting review”

- They encourage you to withdraw your claim

- Your claim is closed without your consent

These patterns show up again and again in cases we handle.

Common Reasons Insurers Drop Policyholders

Insurance companies use claim history, location risk, and repair costs to determine whether you’re still profitable as a customer. When the risk outweighs the premiums they collect, they non-renew policyholders — often right after a damage claim.

When Insurance Companies Cannot Drop You

Texas law prohibits dropping you for:

- Weather-related property claims

- Claims for damage you couldn’t control

- A single glass or towing claim

- Claims older than 3 years

- Discrimination of any kind

If an insurer violates these protections, the law is on your side.

Why Property Damage Claims Trigger More Drops

How Attorneys for Property Damage Protect You After a Claim

Insurance companies drop policyholders after claims because they assume you’ll be expensive later. That’s exactly why working with experienced attorneys for property damage helps level the playing field. Your lawyer identifies improper non-renewals, pushes back against low offers, and holds insurers accountable under Texas law. With the right attorney, you’re not just responding to a claim — you’re protecting your future coverage.

Insurers are far more likely to non-renew after:

- Storm or hail damage

- Home fires

- Burst pipes

- Auto property damage

- Vandalism or theft

Not because of the claim itself—

but because these types of claims might happen again.

We see this pattern constantly when helping clients with

Home Fire Claims

and auto property damage from

car accidents.

Case Study: How We Forced an Insurer to Reverse a Non-Renewal

A Houston homeowner contacted our firm after lightning struck their electrical panel. The insurer paid the initial portion of the claim but then sent a notice refusing to renew the policy, claiming the home no longer met underwriting standards.

Our Steps to Win:

- Reviewed their policy for violations

- Cited Texas Insurance Code non-renewal restrictions

- Sent a formal demand letter for unlawful non-renewal

- Showed the “underwriting” reason was false

- Filed a bad-faith complaint

Outcome:

The insurer immediately reversed the non-renewal and extended coverage.

This is the power of having attorneys for property damage who understand insurer tactics.

How Much Does a Property Damage Attorney Cost?

We keep our fee structure simple. You pay nothing upfront — and you only pay if we win your case. This applies to home damage, auto property damage, storm claims, water leaks, and fire losses.

This applies to property damage, car accident claims, storm damage, home fire claims, and even smaller cases like denied water-leak claims.

Property Damage Types We Handle

We help Texas families with:

- Home fire claims

- Hurricane Damage

- Hail and storm claims

- Water leak + burst pipe claims

- Wind Damage Claims

- Commercial building damage

- Wrongful denial letters

- Delayed payments

- Lowball offers

- Non-renewals after claims

Demand Letter Breakdown: What We Send to Insurers

When homeowners hire attorneys for property damage, one of the first steps we take is preparing a detailed demand letter outlining exactly what the insurer must pay and why.

Our demand letters include:

- Detailed summary of claim

- Legal basis for recovery

- Repair estimates + photos

- Correspondence timeline

- Documentation of delays

- Damages list

- Deadline under Texas law

This creates leverage and forces insurers to take the client seriously.

Checklist: What To Bring to Your Free Case Review

Bringing these items makes your consultation even stronger:

- Photos + videos

- Emails with adjusters

- Receipts

- Policy documents

- Repair estimates

- Letters from the insurer

- Non-renewal notices

Download Our Free Property Damage eBook

Everything Insurance Companies Don’t Want You to Know — In One Free Download

Property damage claims in Texas can get complicated fast. From confusing policy language to lowball offers to being dropped after a claim, most homeowners never get a fair chance because they simply don’t know the rules.

So we created something to fix that.

Get Your FREE Copy: “The Texas Bulldog’s Guide to Property Damage Claims”

Inside this easy-to-read e-book, you’ll learn:

✔ What insurers look for before deciding to drop a customer

✔ How to document your claim the right way

✔ What Texas law requires insurers to do

✔ How to avoid the biggest claim-killing mistakes

✔ How to communicate with adjusters without hurting your case

✔ When to involve an attorney — and how it actually strengthens your claim

✔ What homeowners and drivers should NEVER say to insurance companies

✔ How to spot bad-faith tactics instantly

Why It’s Free

At The Miller Law Firm – Home of The Texas Bulldog, we believe Texans should have real information — not fear, confusion, or pressure from insurance companies.

This guide gives you the tools to protect yourself before your insurer tries to:

- underpay your claim,

- delay your payment, or

- drop you entirely.

How to Protect Yourself After Filing a Claim

To reduce your chances of being dropped:

- Document everything

- Avoid recorded statements

- Follow up regularly

- Keep receipts

- Make temporary repairs

- Review every letter you receive

- Call an attorney before accepting a settlement

If your property loss involves a fire, be sure to review our detailed guide on home fire claims to understand what the insurance adjuster should — and shouldn’t — be doing.

When to Call Attorneys for Property Damage

Call us if:

- Your claim was denied

- Your claim is delayed

- Your settlement is too low

- You received a non-renewal notice

- The adjuster is ignoring you

- The insurer is changing their story

We step in fast and aggressively.

About Adam — The Texas Bulldog

Adam H. Miller, founder of The Miller Law Firm, is widely known as The Texas Bulldog for his relentless approach to fighting insurance companies. He personally oversees every case — no passing clients off to junior associates or case managers — and focuses on protecting Texans who’ve been denied, delayed, or dropped after filing a claim.

Adam’s reputation is built on clear communication, aggressive negotiation, community involvement, and proven results. Whether it’s a home fire, storm damage, burst pipe, or vehicle property loss, Adam brings the experience and determination clients need when insurers stop playing fair.

Adam’s commitment to clients goes beyond the legal work. He’s active in the Houston community, supports local organizations like Big Brothers Big Sisters and Animal Justice League, and is regularly featured in publications like Digital Journal Article and Grit Daily’s How Adam H. Miller Built a Reputation for Relentless Advocacy.

Google Reviews

“Thank you so much they work hard every single day to support clients they are very trusted law firm I am grateful that I chose Miller law firm for there outstanding service they provided. It was a pleasure meeting Adam Miller and his team . Thank you” — Nora S. ⭐️⭐️⭐️⭐️⭐️

“Mr. Miller and his team is very reliable and will listen to every concern you have! They will fight to get the best outcome for you! You are granted to feel like family here. Would high recommend!” — Jae M. ⭐️⭐️⭐️⭐️⭐️

“He was awesome and got things DONE! The staff communicated very well step by step and done things on a swift and timely manner.” — Kefresh ⭐️⭐️⭐️⭐️⭐️

Houston Property Damage Lawyer | Fighting Insurance Claim Denials

Frequently Asked Questions for Attorneys for Property Damage

Can insurance drop me after a not-at-fault accident?

Yes. Some insurers still non-renew drivers even when they didn’t cause the crash.

Can homeowners insurance drop me after storm damage?

Not in the first 12 months. And never for a natural disaster that wasn’t your fault.

Is non-renewal the same as cancellation?

No. Cancellation ends a policy mid-term. Non-renewal ends it at the expiration date.

Can attorneys help reverse a non-renewal?

Yes. We’ve forced insurers to reverse unlawful drops many times.

What happens if I file a claim and then get dropped?

Your coverage stays active until the end of your policy period, but you may face difficulty finding affordable replacement insurance. An attorney can often challenge the non-renewal or help reverse it.

Will my premiums increase after a property damage claim?

Yes, most insurers raise rates after a claim — even if it wasn’t your fault. The amount depends on the claim type, repair cost, and your prior claim history.

How long after a claim can an insurance company non-renew me in Texas?

They cannot non-renew you during the first 12 months of a new policy. After that period, they can only non-renew for legally valid reasons — not for weather-related claims or claims outside your control.

Google Map – The Miller Law Firm

4900 Woodway Drive, Suite 900

Houston, TX 77056