Homeowners in Texas face unique risks. From hurricanes along the Gulf Coast to hailstorms, flooding, and even winter freezes, property damage is a fact of life for many. While home insurance is meant to protect you from devastating financial loss, many families learn the hard way that insurance companies don’t always honor their promises.

That’s where lawyers for home insurance claims step in. At The Miller Law Firm – home of The Texas Bulldog, we fight for homeowners across Houston and throughout Texas who have had their legitimate claims delayed, underpaid, or denied. This article will walk you through what Texas insurance law requires, the most common disputes we see, and how an attorney can help you maximize your recovery.

Understanding Home Insurance Laws in Texas

Texas insurance laws are designed to protect policyholders, but the language is often technical and confusing. Here are key takeaways every homeowner should know:

- Prompt Payment of Claims Act (Texas Insurance Code Chapter 542): Insurance companies must acknowledge, investigate, and accept or deny claims within strict timelines. Delays can trigger financial penalties.

- Bad Faith Protections: Texas law prohibits insurers from engaging in unfair practices like misrepresenting policy language, failing to conduct a reasonable investigation, or refusing to pay without a valid reason.

- Statutory Interest and Attorney’s Fees: If your insurer violates the law, you may be entitled to 18% annual interest plus attorney’s fees on top of your claim payment.

- Homeowners’ Rights: You have the right to see your full policy, receive a prompt and fair investigation, and appeal denials.

Internal link: We cover this in more detail in How Do I Fight a Denied Insurance Claim?.

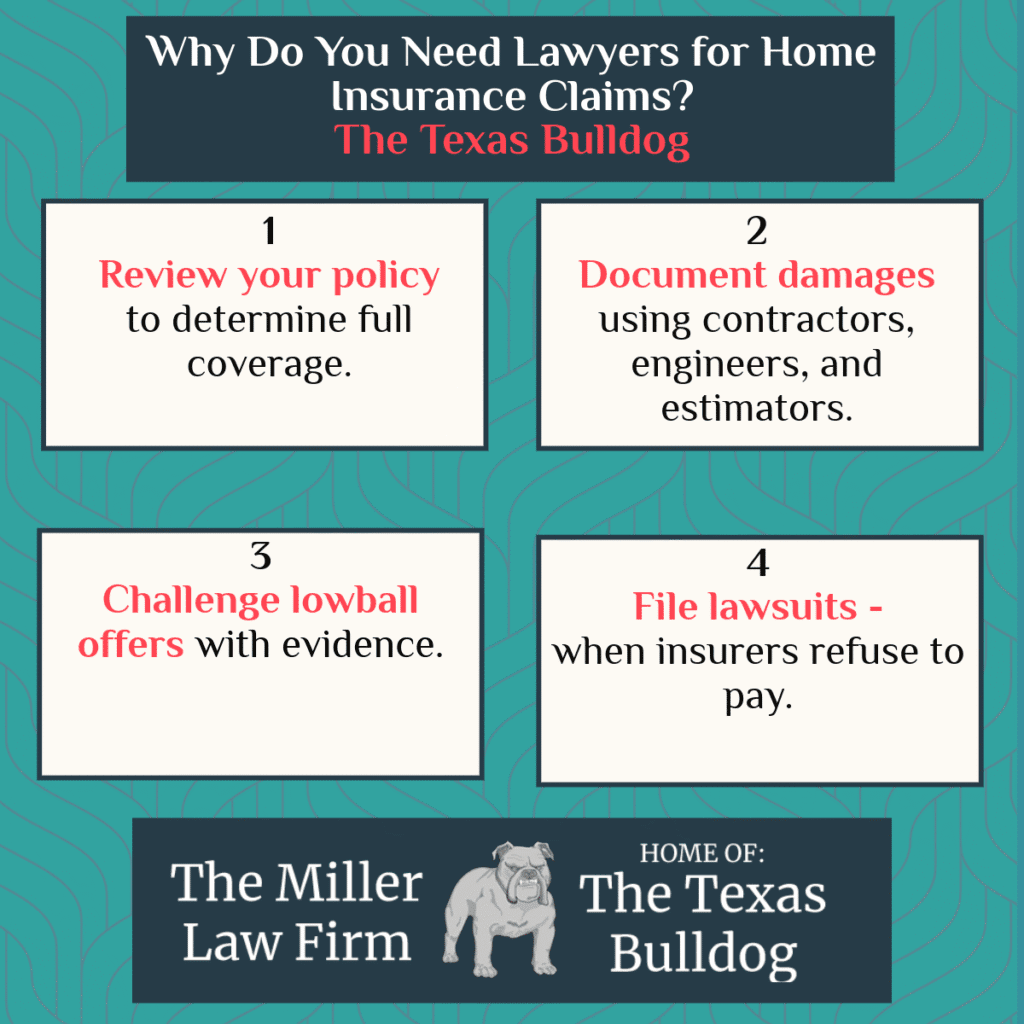

Why Do You Need Lawyers for Home Insurance Claims?

Insurance adjusters are trained to minimize payouts. Hiring an attorney levels the playing field. A skilled lawyer can:

- Review your policy to determine full coverage.

- Document damages using contractors, engineers, and estimators.

- Challenge lowball offers with evidence.

- File lawsuits when insurers refuse to pay.

Many of our clients come to us after trying to handle claims alone. Learn more in Property Damage Claims: Home Fire Claims.

Common Types of Home Insurance Disputes in Texas

- Hail and Windstorm Damage – Common across Houston suburbs and Gulf Coast counties.

- Hurricane Claims – Insurers often argue pre-existing damage or improper maintenance.

- Water Damage and Burst Pipes – Particularly after Winter Storm Uri, thousands of claims were challenged.

- Fire and Smoke Damage – Losses are often undervalued.

- Theft and Vandalism – Insurers sometimes question proof of ownership.

Internal link: If you’re dealing with hurricane or storm damage, see our Hurricane Damage Claims Guide.

What Are Flood Prone Properties in Houston?

Flooding is one of the biggest risks facing Houston homeowners. According to FEMA, properties are classified into flood zones that determine insurance requirements and premiums:

- Zone AE: Areas at high risk of flooding, often along bayous and creeks.

- Zone VE: Coastal flood zones subject to storm surge.

- Zone X (shaded): Moderate risk zones.

- Zone X (unshaded): Minimal risk zones.

Neighborhoods like Meyerland, Greenspoint, and areas along Brays Bayou have historically been among the most vulnerable. Homeowners in these zones may be required to carry separate flood insurance through the National Flood Insurance Program (NFIP).

Internal link: Learn more about Which Month Has the Most Hurricanes in Texas?

Steps to Take After a Property Damage Loss

- Document Everything – Take photos and videos immediately.

- Notify Your Insurer Promptly – Delays can harm your claim.

- Keep All Receipts – For repairs, hotels, and living expenses.

- Get Professional Help – Don’t rely only on your insurer’s adjuster.

Internal link: We explain this further in Everything You Need to Know About Auto Insurance (helpful for multi-policy households).

How Insurance Companies Deny or Delay Claims

Insurance companies use many tactics to avoid paying:

- Claiming the damage is “wear and tear.”

- Arguing that maintenance issues caused the problem.

- Offering a fraction of repair costs.

- Dragging out the investigation process.

Internal link: See how we’ve helped in Slip and Fall Blog Post — insurers use the same delay tactics in injury claims.

What Are the Insurance Laws in Texas: Key Protections for Homeowners

- Texas Insurance Code Chapter 541: Prohibits deceptive practices.

- Chapter 542 (Prompt Payment): Requires strict timelines.

- Texas Deceptive Trade Practices Act (DTPA): Adds further consumer protections.

- Case Law: Courts have upheld homeowners’ rights to full, timely payments.

Texas Home Insurance vs Flood Insurance

| Coverage Type | What It Covers | Common Exclusions | Who Provides It? |

|---|---|---|---|

| Homeowners Insurance | Fire, wind, hail, theft, liability, some water damage | Flooding, earthquakes, mold, neglect | Private insurance companies |

| Flood Insurance | Rising water, storm surge, FEMA flood events | Wind damage, sewer backups (unless added) | National Flood Insurance Program (NFIP) |

People Also Ask (FAQ)

How long does an insurance company have to settle a claim in Texas?

Generally, insurers must acknowledge a claim within 15 days, request documents within 15 days, and accept or deny within 15 business days after receiving proof.

Can I sue my insurance company in Texas?

Yes. Texas law allows you to sue for breach of contract, bad faith, or violations of the Insurance Code.

What damages can I recover if my insurer acts in bad faith?

You may recover the claim amount, attorney’s fees, 18% annual interest, and sometimes additional damages.

Do I need flood insurance in Houston?

If you live in a high-risk FEMA flood zone and have a federally backed mortgage, flood insurance is required. Even in “low-risk” zones, coverage is strongly recommended.

What is considered bad faith in Texas insurance law?

Examples include denying claims without investigation, misrepresenting policy terms, and unreasonable delays.

Additional Homeowners Insurance FAQ

Does Texas law require homeowners insurance?

Texas law does not require it, but lenders usually do.

What are the most common home insurance exclusions?

Flood, mold, earthquake, and maintenance issues are often excluded unless you buy additional coverage.

How much does a lawyer for home insurance claims cost in Texas?

Most work on a contingency fee basis, meaning no upfront costs—you only pay if you win.

What if my insurance company lowballs my repair estimate?

Hire an independent estimator and contact a lawyer immediately.

Can I switch insurers after filing a claim?

Yes, but your claims history will follow you and may impact premiums.

Does Texas have a Homeowner’s Bill of Rights?

Yes. Texas law protects homeowners with rights to prompt payment of claims, transparency in policy language, and freedom from unfair claim handling practices.

What happens if insurance won’t pay for water damage in Texas?

It depends on the cause. Sudden and accidental water damage (like burst pipes) is usually covered, while gradual leaks or flood water often are not. You may need a lawyer to challenge wrongful denials.

What are my rights if my insurance company delays payment?

Under the Texas Prompt Payment of Claims Act, insurers must act within specific timelines. If they don’t, they can owe 18% interest per year plus attorney’s fees.

Does homeowners insurance cover mold damage in Texas?

Not always. Standard policies often exclude mold unless it results from a covered peril (like water damage from a burst pipe). Additional endorsements may be required.

How can a lawyer help me with a denied flood damage claim?

An attorney can investigate FEMA flood zone classifications, challenge improper exclusions, and hold insurers accountable under Texas law for unfair denials.

Why Choose The Miller Law Firm – The Texas Bulldog

When insurers try to deny, delay, or underpay, we bite back. Our reputation in Houston and across Texas is built on tough advocacy and real results. We’ve stood up to some of the largest insurance companies in the nation and won millions for policyholders.

👉 Related Content: 10 Essential Insurance Tips for Texas Homeowners

Contact The Texas Bulldog Today

If your home insurance claim has been delayed or denied, don’t fight alone. Call The Miller Law Firm – home of The Texas Bulldog today at 713-572-3333 for a free consultation. Let us fight to get you the coverage you paid for and the compensation you deserve.

👉 See what past clients say about us on Google Reviews. ⭐ Rated 4.9/5 by Houston homeowners for property damage and home insurance claim representation.