Living in Texas, homeowners face a wide array of natural threats—from flooding and hurricanes along the Gulf Coast to tornadoes in the Panhandle and hailstorms in the Hill Country. But many Texas homeowners assume their standard home insurance will cover all of these hazards. In reality, quite a few natural disasters are excluded from ordinary home insurance policies.

This article dives deep into what natural disasters are not covered by home insurance in Texas, why those gaps exist, what supplemental coverages you should consider, and how a property damage attorney (like the ones at Texas Bulldog Law) can assist when insurers deny or underpay claims. We’ll also highlight internal resources on hail claims, water damage, and insurance tips for Texas homeowners to help you build the strongest protection plan possible.

Table of Contents

- What Standard Texas Homeowners Insurance Usually Covers (and What It Doesn’t)

- Natural Disasters Often Excluded from Texas Homeowners Insurance

- Why Do These Gaps in Coverage Exist?

- Which Natural Disasters Are Covered?

- How to Fill the Gaps: Supplemental Coverages & Insurance Add-Ons

- What to Do After a Natural Disaster: Claims, Documentation & Legal Help

- State & Federal Programs: TWIA, NFIP & TDI Protections

- Real-World Examples & Case Studies

- Tips for Homeowners to Strengthen Protection

- Download our free Property Damage eBook

- Conclusion & Next Steps

- Contact The Texas Bulldog

What Standard Texas Homeowners Insurance Usually Covers (and What It Doesn’t)

First, it’s important to understand the baseline. A typical Texas homeowners insurance policy (HO-3 form or equivalent) will cover certain risks (called perils), but not everything. According to the Texas Department of Insurance, standard policies typically include coverage for fire, lightning, theft, and sometimes wind and hail (depending on your location).

However, there are important limitations:

- Deductibles: Many Texas policies use percentage-based deductibles for storm or hail damage—meaning you must pay a percentage of your home’s insured value before the policy pays anything.

- Excluded perils: Standard policies do not cover everything. Common exclusions include floods, earthquakes, landslides, sinkholes, mold, wear and tear, and damage from pests or insects.

- Windstorm / hurricane zones: In many coastal counties in Texas, insurers exclude windstorm and hail damage from standard policies. In those cases, you must obtain a separate windstorm policy or get coverage via the Texas Windstorm Insurance Association (TWIA).

So the question becomes: Which natural disasters do homeowners often assume are covered but actually are not? Let’s explore each in depth.

Natural Disasters Often Excluded from Texas Homeowners Insurance

Below is a comprehensive breakdown of major natural disasters and whether they are covered—or more importantly, not covered—by standard home insurance in Texas.

1 Floods and Storm Surge

Not covered by standard home insurance. Floods remain one of the most common disasters denied under typical home policies.

Why not covered?

Flood damage can spread across multiple properties, creating catastrophic losses that insurers would struggle to absorb. As a result, flood insurance is handled separately—usually through the National Flood Insurance Program (NFIP) or private flood insurance.

Important nuance: If wind or hail damages your roof (a covered peril) and rain then enters, your homeowners policy might cover the resulting interior damage (water infiltration). But damage from surface flooding, storm surge, river overflow, or groundwater seepage is usually excluded.

Example scenario: A hurricane pushes storm surge into your home’s first floor. Even though the storm is “natural,” the flood component won’t be covered under your homeowners policy.

2 Earthquakes & Earth Movement

Excluded in standard policies. Most homeowners insurance policies specifically exclude damage caused by earth movement, including earthquakes, landslides, sinkholes, mudflows, and subsidence.

If you live in a region with seismic activity or risk of ground shifting (e.g. due to fracking, mining, or soil issues), you’ll need a separate earthquake or earth movement endorsement.

3 Sinkholes, Landslides, and Subsidence

These are typically excluded, unless you purchase special add-ons. A standard home insurance policy will almost always deny claims arising from ground collapse or shifting soil.

If you live in an area prone to sinkholes or land movement, ask your agent whether you can add a rider or endorsement to cover these perils.

4 Hurricanes / Windstorm in High-Risk Zones (without specific coverage)

Though many standard policies do provide wind and hail coverage, in coastal Texas and high-risk hurricane / windstorm zones, insurers often exclude windstorm and hurricane damage from the base policy. Homeowners must purchase a standalone windstorm policy or obtain wind coverage from a specialized insurer or TWIA.

For instance, a home in Galveston or Corpus Christi might need TWIA coverage because private insurers exclude wind damage in those areas.

Even with wind coverage, storm surge and flood damage from a hurricane still require separate flood insurance. See our Houston Homeowners’ Guide to Post-Hurricane Berryl Property Recovery

5 Tornadoes (Partially Covered, Subject to Limitations)

Tornado damage is generally covered under standard home insurance if wind damage is included. However, this depends on your insurance company and whether your location has windstorm exclusions.

- If your policy includes wind / hail coverage, tornadoes (being wind events) may be covered.

- But in regions where windstorm is excluded (coastal or hurricane-prone zones), tornado damage might also be excluded.

- Even when covered, your policy might impose a storm deductible (percentage‐based) that significantly limits what you recover.

So while tornadoes are often covered, be cautious: they may carry higher deductibles or exclusions depending on location.

6 Wildfires / Structural Fire (Covered, but some “natural fires” edge cases excluded)

Generally, home fires and wildfire damage are part of standard coverage. But there are exceptions:

- If fire damage arises from a nuclear event, war, or some government action, those are excluded.

- Also, smoke damage tied to an excluded peril may be denied.

- If a wildfire starts due to an excluded cause (e.g. arson, negligence), insurers may deny claims.

Fire is usually a core coverage—but always check the “exclusions” section.

7 Mold, Rot, and Wear & Tear (Not “Natural Disasters” but Common Exclusions)

While not always classified as “natural disasters,” many claims resulting after storms run into exclusions like mold, gradual water damage, or wear and tear:

- Standard policies exclude damage from mold or fungus unless directly tied to a covered peril.

- Deterioration from long-term leaks, aging roofs, or lack of maintenance is typically excluded.

- Infestations by insects, rodents, or pests are excluded, even if worsened by storm damage.

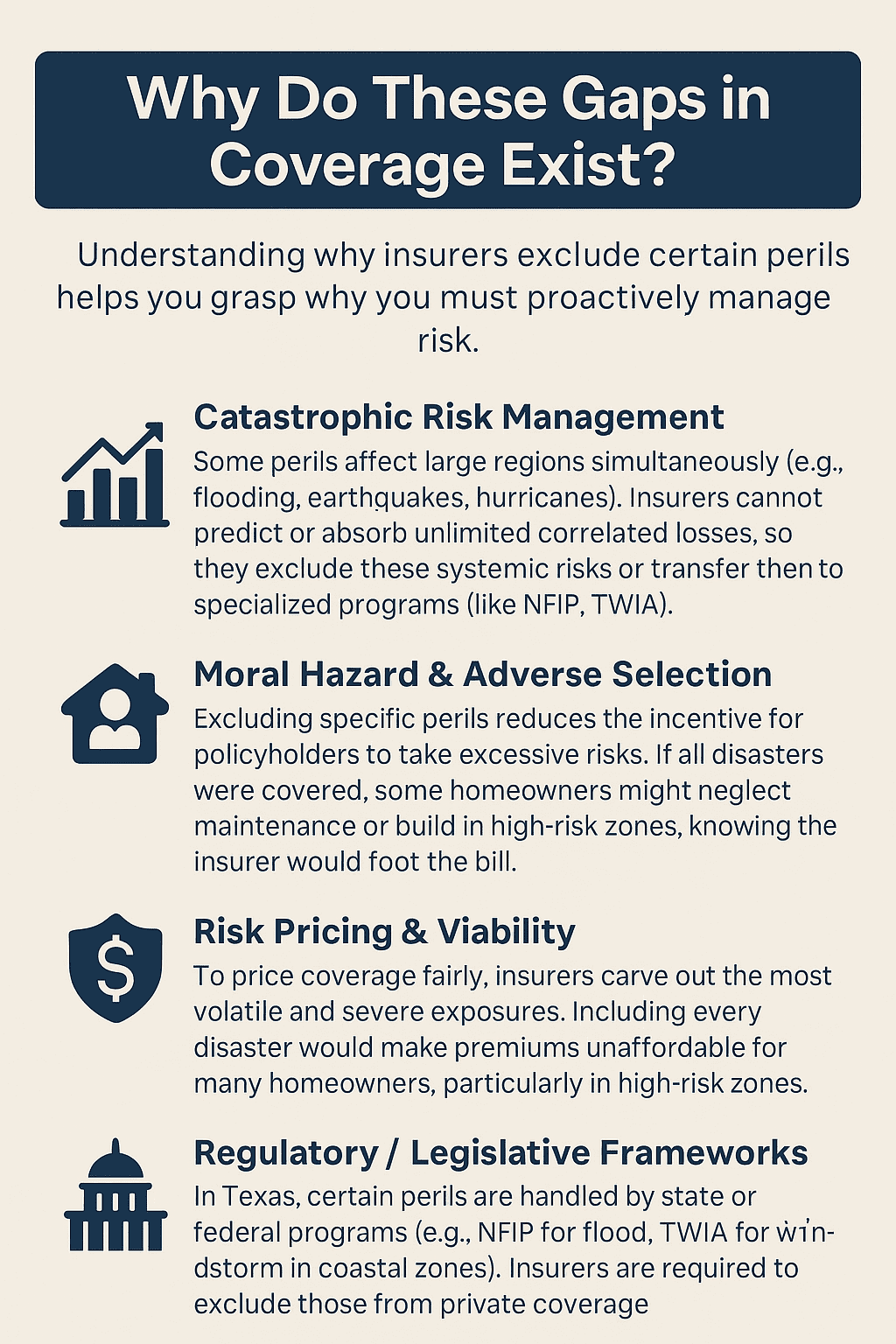

Why Do These Gaps in Coverage Exist?

Which Natural Disasters Are Covered (So You Know the Boundaries)

Before diving into what’s excluded, here’s a quick list of risks commonly covered by standard home insurance in many Texas policies:

- Fire and smoke damage

- Theft and vandalism

- Wind and hail (if the policy includes it)

- Damage from falling trees or branches

- Water damage from burst pipes (internal plumbing)

- Certain liability and medical payments

But again: these coverages come with limitations, conditions, and sometimes expensive deductibles.

How to Fill the Gaps: Supplemental Coverages & Insurance Add-Ons

Knowing what’s excluded is only half the battle. Here’s how Texas homeowners can proactively protect themselves:

Flood Insurance (NFIP or Private)

To protect against flood or storm surge damage, purchase a flood insurance policy. Most homeowners get this via the National Flood Insurance Program (NFIP), but some private flood insurers now offer competitive alternatives.

Be aware of waiting periods: NFIP typically has a 30-day waiting period before coverage becomes active.

Earthquake / Earth Movement Endorsements

If you live near fault lines or in areas with ground instability, ask your insurer whether you can add an earthquake endorsement, or purchase a standalone earthquake policy.

Windstorm & Hurricane Policies (or TWIA for Coastal Zones)

In coastal or high-risk wind zones, your standard home insurance may exclude windstorm damage. In that case:

- Get a standalone windstorm/hurricane policy

- If you reside in a coastal county eligible for TWIA, consider TWIA coverage. TWIA is the state-backed insurer of last resort for windstorm and hail in assigned areas.

- Ensure your home has a certificate of compliance (WPI-8 or WPI-8E/WPI-8C) to qualify.

Endorsements for Sinkholes, Landslides, and Ground Movement

Some insurers offer add-ons or endorsements for otherwise excluded perils such as ground collapse or sinkholes. These vary widely in cost and availability.

Umbrella Policies or Excess Liability

While an umbrella policy doesn’t typically expand property perils, it can provide additional liability coverage if someone is injured on your premises during or after a disaster.

What to Do After a Natural Disaster: Claims, Documentation & Legal Help

Knowing what’s excluded is important—but what really matters is what you do when disaster strikes.

Immediate Steps After Damage

- Ensure safety first — evacuate or shelter as needed.

- Document everything — photographs, videos, dated logs of events.

- Prevent further damage — board up windows, tar roof, cover broken walls.

- Notify your insurer quickly — follow timelines specified in your policy.

- Save receipts — for emergency repairs, accommodations, and temporary expenses (often reimbursable under Additional Living Expenses, or ALE).

What Insurers May Do (or Deny)

Insurers often deny or underpay claims based on exclusions, causation (e.g. was damage from excluded flood, or from covered wind), or insufficient documentation. In coastal zones, insurers may shift wind claims to TWIA or reject them altogether if coverage was excluded.

If your insurer improperly denies, delays, or undervalues a claim, you can escalate:

- Request appraisal or independent evaluation

- File a complaint with Texas Department of Insurance (TDI)

- Hire a property damage / insurance dispute attorney (such as those at The Miller Law Firm)

Our Property Damage Claims page at Texas Bulldog Law outlines how we represent homeowners in disputes over hail, wind, water, hurricane, and fire damages.

If your claim involves water damage (e.g., flood infiltration or pipe bursts), also check our Water Damage Claims Texas page for insights and legal steps.

Additionally, if your home sustains hail damage, our firm handles many such cases; see our Hail Storm Property Damage Lawyer in Houston page.

State & Federal Programs: TWIA, NFIP & TDI Protections

1 TWIA (Texas Windstorm Insurance Association)

In many Texas coastal counties, insurers exclude windstorm and hail from standard policies. TWIA exists as a state-backed insurer of last resort for wind and hail coverage in those zones.

Key points:

- To qualify, the property often must be denied by at least one private insurer.

- The property must generally comply with building codes and have a compliance certificate.

- TWIA policy covers wind and hail, but not flood or surge.

- Coverage limits and premiums are set annually and may vary.

2 NFIP (National Flood Insurance Program)

For flood coverage, Texas homeowners often rely on NFIP. It is backed by the federal government, offering policies even when private flood insurance is unavailable.

3 Texas Department of Insurance (TDI)

If you experience an insurance dispute, you can file a consumer complaint with TDI. They have regulatory oversight and can investigate insurer behavior.

TDI also publishes tips and FAQs for homeowner coverage and disaster claims.

Real-World Examples & Case Studies

Coastal Home vs Inland Home

- Coastal property (e.g. Port Arthur, Galveston): Likely needs separate windstorm coverage or TWIA + flood insurance. Without those, hurricane wind damage and storm surge damage would be denied.

- Inland property (e.g. Austin, Dallas): Standard policy often covers wind, hail, tornado – but excludes flood, earthquake, and ground movement, so you’ll want to add flood or earthquake where necessary.

Recent Kerr County Flood (2025)

A Houston Chronicle investigation found that less than 5% of homes in high-risk flood areas in Kerr County had flood insurance ahead of a major July 4 flood. Many homeowners were hit with devastating losses not covered by their homeowners policies.

This underscores how flood exclusion is a real, costly gap—even in inland and “unexpected” flood zones.

Tips for Homeowners to Strengthen Protection

- Review your policy’s perils and exclusion sections thoroughly. Don’t rely on verbal assurances.

- Calculate your storm deductibles—especially percentage deductibles. If your house is insured for $400,000 with a 2% storm deductible, your out-of-pocket is $8,000.

- Consider flood insurance even if your home isn’t in a high-risk zone. Many floods arise outside FEMA-mapped areas.

- If in coastal or wind-prone zones, buy windstorm / hurricane coverage or check TWIA eligibility.

- Add endorsements (earthquake, sinkhole) if available in your region.

- Document all property condition and improvements—keep photos, receipts, and records to support future claims.

- Inspect and maintain your property—damage caused by neglect or deferred maintenance is usually denied.

- Consult an attorney early if your insurer denies or undervalues a claim.

We discuss more of these insurance tips in our blog “10 Essential Insurance Tips for Texas Homeowners” on Texas Bulldog Law.

Download our free Property Damage eBook

Conclusion

Understanding what natural disasters are not covered by home insurance in Texas is critical for protecting your most valuable asset. While standard policies often cover fires, theft, and sometimes wind and hail, they exclude major perils like flooding, earthquakes, sinkholes, and windstorm/hurricane in certain zones—unless you carry supplemental coverage.

If you live near the coast, invest in TWIA or windstorm policies. If your area is flood-prone, get flood insurance. And if you live in zones susceptible to ground movement, ask about endorsements for earth collapse or subsidence.

When disaster strikes, document everything, notify your insurer, and don’t hesitate to lean on legal counsel. Our Property Damage Claims, Hail Storm Property Damage Lawyer, and Water Damage Claims pages provide helpful next steps and examples specific to Texas.

At Texas Bulldog Law, we specialize in helping homeowners navigate insurance disputes after storms, floods, and property damage. If your insurer refuses to pay or undervalues your claim, contact us for a free consultation—we’ll fight to get you the full compensation you’re owed.

Contact The Texas Bulldog

At The Miller Law Firm – Home of The Texas Bulldog, we measure success not just by the results we deliver, but by the impact we have on our clients’ lives. Here’s what recent clients have said about working with us:

Cynthia Newsom ⭐⭐⭐⭐⭐

“I love him. He took very good care of me and I would recommend him to anybody who needs help.”

Oneal Thompson ⭐⭐⭐⭐⭐

“Thank you so much! Your kindness and patience with me when I was impatient, yes I had plenty of financial fears going into this. The relief that ALL my medical bills were paid and I still walked away with money made it all worth it! Erica and Julia were awesome! God bless you all.”

Miriam H ⭐⭐⭐⭐⭐

“Excellent barratry attorney! The Texas Bulldog got me a settlement from an individual who illegally solicited me after a car accident and it only took a few months.”

The Miller Law Firm has won hundreds of millions for our clients and is well known as one of the best firms in Houston. However, don’t just take our word for it. Check out our 100+⭐⭐⭐⭐⭐5 Star Reviews on Google! Contact us now for a free, no-obligation case review.